Comparing U.S. High-Yield Savings Accounts: Finding the Best Rates Above 5% for 2026

Anúncios

Are your savings working hard enough for you? When it comes to Comparing U.S. High-Yield Savings Accounts, finding the right home for your money can mean the difference between pennies and serious passive income.

With the Federal Reserve holding interest benchmarks steady, certain online banking platforms and digital credit unions are still aggressively competing for your deposits.

Anúncios

These institutions are offering premium annual percentage yields that leave traditional brick-and-mortar returns in the dust.

Navigating this changing financial landscape requires a clear look at which top-tier growth vehicles actually deliver on their promises. Here is our objective breakdown of the standout platforms helping you maximize your compound interest and protect your purchasing power this year.

The Evolving Landscape of High-Yield Savings Accounts for 2026

The financial markets are dynamic, with interest rates constantly adjusting to economic pressures and central bank decisions. For individuals seeking to optimize their savings, staying informed about these movements is not just beneficial, but essential to capitalize on opportunities.

Experts anticipate continued volatility but also potential stability in rates as the economy progresses towards 2026. This period presents a unique window for consumers to lock in attractive returns on their deposits, especially through high-yield savings accounts.

Anúncios

Understanding the factors that influence these rates—such as inflation, Federal Reserve policy, and bank competition—is crucial for anyone focused on Comparing U.S. High-Yield Savings Accounts.

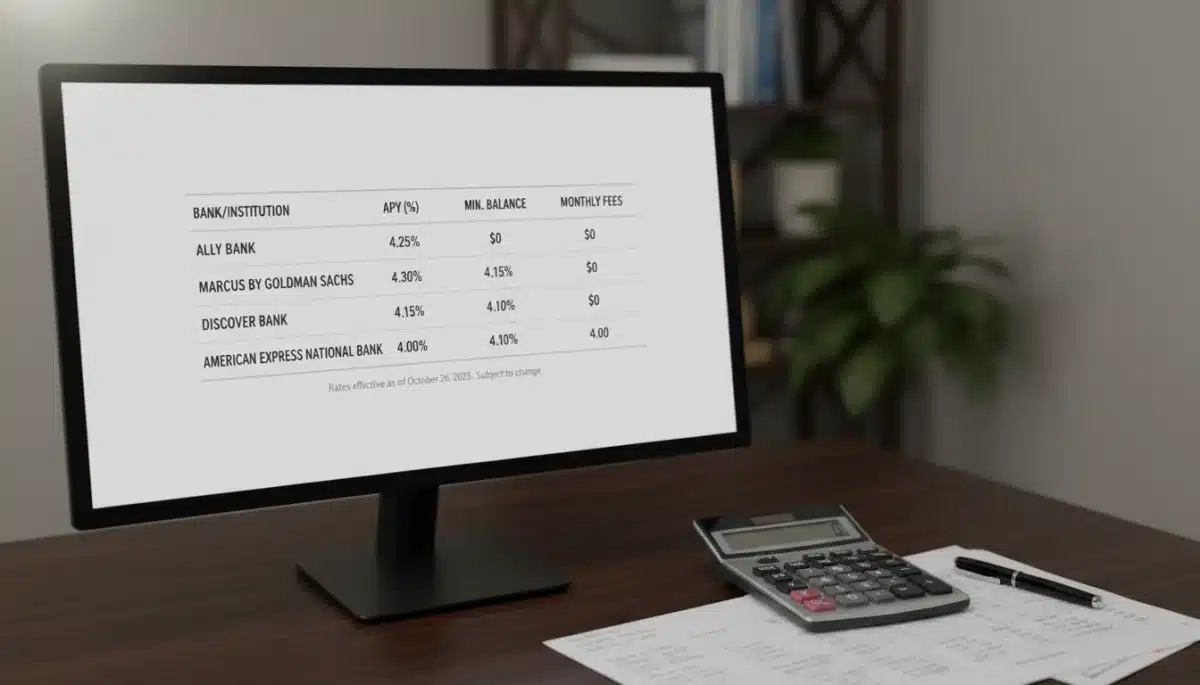

Identifying Top Contenders: Accounts Exceeding 5% APY

Several financial institutions are currently offering or are projected to offer annual percentage yields (APYs) exceeding 5% on their high-yield savings accounts.

These often include online-only banks and credit unions, which typically have lower overhead costs, allowing them to pass on higher interest rates to their customers.

These institutions are actively competing for deposits, making it a favorable environment for savers diligently Comparing U.S. High-Yield Savings Accounts.

Key considerations beyond just the APY include minimum balance requirements, fee structures, and withdrawal limitations.

Consumers should carefully review the terms and conditions of each account to ensure it aligns with their financial habits and liquidity needs.

The goal is not just to find a high rate, but one that fits seamlessly into your overall financial strategy for high-yield savings accounts 2026.

Key Institutions to Watch

- Online Banks: Often lead with the most competitive rates due to reduced operating costs.

- Credit Unions: Member-owned structures can sometimes offer higher dividends to their members.

- Fintech Platforms: Innovative solutions sometimes partner with banks to offer attractive savings products.

While brick-and-mortar banks may offer convenience, their high-yield offerings typically lag behind their online counterparts. This disparity is a critical point when Comparing U.S. High-Yield Savings Accounts.

It is important to verify that any chosen institution is FDIC-insured, protecting your deposits up to $250,000 per depositor, per institution, in case of bank failure. This federal backing provides a vital layer of security for your funds.

Factors Driving High-Yields: Economic Influences and Federal Reserve Policy

The current high-yield environment is largely a result of the Federal Reserve’s monetary policy decisions, particularly its efforts to combat inflation. When the Fed raises its benchmark interest rate, banks often follow suit by increasing their savings rates to attract deposits.

Inflation rates also play a significant role; higher inflation erodes purchasing power, making higher savings rates more appealing and necessary for consumers. This economic backdrop creates favorable conditions for Comparing U.S. High-Yield Savings Accounts..

Market competition among banks further drives up rates, as institutions vie for customer funds. This competitive dynamic is a boon for savers, pushing APYs upward across the board for high-yield savings accounts 2026.

Looking ahead to 2026, analysts suggest that while the Fed may eventually ease its rate hikes, rates could remain elevated for some time. This forecast underscores the opportunity presented by Comparing U.S. High-Yield Savings Accounts.

Consumers should monitor economic reports and Federal Reserve announcements closely. These indicators provide valuable insights into potential rate shifts and help in making timely financial decisions regarding high-yield savings accounts.

Beyond the APY: What Else to Consider When Choosing an Account

While a high APY is undoubtedly the primary draw, a thorough evaluation of high-yield savings accounts requires looking beyond just the interest rate. Other features can significantly impact the overall value and suitability of an account for your needs.

Accessibility to funds is a critical factor. Some high-yield accounts may impose limitations on the number of withdrawals per month or require specific transfer methods, which could affect your liquidity. This is a key aspect when Comparing U.S. High-Yield Savings Accounts.

Understanding the fee structure is also paramount. Hidden fees for maintenance, transfers, or early withdrawals can quickly diminish the benefits of a high interest rate, making a seemingly attractive offer less appealing for high-yield savings accounts 2026.

Essential Features to Evaluate

- FDIC Insurance: Ensures your deposits are protected by the U.S. government.

- Minimum Balance Requirements: Some accounts require a certain balance to earn the advertised APY or avoid fees.

- Linked Checking Accounts: Offers seamless transfers and management of funds.

- Customer Service: Responsive and accessible support can be invaluable for managing your account.

Digital tools and mobile app functionality also play a role in convenience. A well-designed app can make managing your high-yield savings account effortless, allowing you to track interest earnings and transfer funds with ease.

For those focused on Comparing U.S. High-Yield Savings Accounts, a holistic approach to evaluation will yield the best long-term results. It’s about finding the right balance between rate and functionality.

Maximizing Your Returns: Strategies for High-Yield Savings

Simply opening a high-yield savings account is the first step; actively managing it can further enhance your returns. One strategy involves regularly reviewing your account’s APY against market trends to ensure you’re always getting the best available rate.

Consider setting up automatic transfers from your checking account to your high-yield savings account. This consistent savings habit can significantly boost your balance over time, leveraging the power of compound interest for high-yield savings accounts 2026.

For those with significant savings, spreading funds across multiple FDIC-insured institutions can offer additional protection and potentially higher combined returns. This diversified approach is smart when Comparing U.S. High-Yield Savings Accounts.

It is also beneficial to understand how interest is calculated and compounded. Accounts that compound interest daily often yield slightly more over time than those that compound monthly or quarterly, a small but impactful detail for high-yield savings accounts.

Staying disciplined and avoiding unnecessary withdrawals will ensure your money grows as efficiently as possible. The goal is to let your savings work for you, accumulating substantial interest as you approach 2026 and beyond.

The Role of Online-Only Banks in High-Yield Offerings

Online-only banks have emerged as significant players in the high-yield savings market, consistently offering more competitive rates than traditional brick-and-mortar institutions.

Their lower operational costs, free from the expenses of physical branches, allow them to pass these savings on to customers in the form of higher APYs.

This model has fundamentally reshaped the banking landscape, providing consumers with unprecedented access to attractive savings opportunities.

For anyone Comparing U.S. High-Yield Savings Accounts: Finding the Best Rates Above 5% for 2026, online banks are often the first place to look.

The convenience of managing accounts entirely online, often through intuitive mobile apps, also appeals to a broad demographic. This digital-first approach aligns with modern financial habits, making high-yield savings accounts 2026 more accessible than ever.

Advantages of Online Banks

- Higher Interest Rates: Generally offer superior APYs compared to traditional banks.

- Lower Fees: Many online accounts come with no monthly maintenance fees.

- Accessibility: Manage your money 24/7 from anywhere with an internet connection.

While some consumers may initially be hesitant about banking without physical branches, the security and reliability of established online banks are on par with traditional institutions. All reputable online banks are FDIC-insured, offering the same level of protection.

The ongoing trend favors digital banking solutions, and this is particularly evident in the high-yield savings sector. Therefore, a comprehensive search for high-yield savings accounts 2026 must heavily consider online options.

Government Regulations and Consumer Protection

When engaging with high-yield savings accounts, understanding the regulatory framework is crucial for consumer protection.

The Federal Deposit Insurance Corporation (FDIC) plays a vital role, insuring deposits up to $250,000 per depositor, per insured bank, for each account ownership category.

This insurance provides a critical safety net, assuring depositors that their money is secure even if an FDIC-insured institution fails. Verifying FDIC membership is a non-negotiable step for anyone Comparing U.S. High-Yield Savings Accounts.

Additionally, federal regulations, such as those implemented by the Consumer Financial Protection Bureau (CFPB), aim to ensure transparency and fairness in banking practices. These protections safeguard consumers from predatory fees and misleading terms in high-yield savings accounts.

Consumers should always review the fine print and terms and conditions provided by banks. Understanding withdrawal limits, fee schedules, and how interest is calculated can prevent unexpected surprises and ensure the account truly serves your financial interests.

Staying informed about regulatory changes and consumer rights empowers individuals to make confident choices when selecting high-yield savings accounts. This vigilance is key to a secure and profitable savings strategy for high-yield savings accounts 2026.

Anticipating 2026: Future Outlook for High-Yield Savings

As we project forward to 2026, the outlook for high-yield savings accounts remains cautiously optimistic, though subject to the broader economic climate.

While the Federal Reserve’s rate-hiking cycle may slow, interest rates could stabilize at levels favorable to savers, maintaining attractive APYs.

Technological advancements are also expected to continue influencing the market, with more innovative digital banking solutions emerging. These innovations could lead to even more competitive offerings and enhanced user experiences for high-yield savings accounts.

Economic growth, inflation trends, and global financial stability will all play a part in shaping the interest rate environment. Consumers should remain adaptable and continue to monitor market conditions to take advantage of the best opportunities when Comparing U.S. High-Yield Savings Accounts.

The competitive nature of the banking industry is likely to persist, ensuring that institutions will continue to vie for deposits. This sustained competition is a positive sign for savers looking for robust returns on their high-yield savings accounts.

Ultimately, a proactive and informed approach will be the most effective strategy for maximizing savings in the coming years. Regular review and adjustment of your savings strategy will ensure sustained financial growth.

| Key Aspect | Brief Description |

|---|---|

| Current Rate Environment | Driven by Fed policy, offering competitive APYs above 5%. |

| Key Account Features | Look beyond APY to fees, minimums, and FDIC insurance. |

| Online Banks’ Role | Often provide highest rates due to lower operational costs. |

| Future Outlook 2026 | Rates likely to remain favorable, requiring ongoing monitoring. |

Frequently Asked Questions About High-Yield Savings

A high-yield savings account typically offers an interest rate significantly higher than traditional savings accounts. These accounts are usually found at online banks and are designed to maximize earnings on deposited funds, often with competitive annual percentage yields (APYs).

Yes, as long as the institution is FDIC-insured. The Federal Deposit Insurance Corporation (FDIC) protects your deposits up to $250,000 per depositor, per insured bank, for each account ownership category, providing a robust safety net.

To find the best rates, regularly compare offers from various online banks and credit unions. Focus on institutions that consistently offer competitive APYs, minimal fees, and favorable terms. Monitoring financial news and comparison sites can also help.

Several factors influence these rates, including the Federal Reserve’s benchmark interest rate, inflation levels, and competition among banks. Economic conditions play a significant role in determining how attractive high-yield savings accounts become to consumers.

Absolutely. Fees can quickly erode your interest earnings. Always check for monthly maintenance fees, withdrawal fees, and other hidden charges. Opt for accounts with transparent, low-cost structures to maximize your overall return on high-yield savings accounts.

Looking Ahead: Strategic Savings for 2026

The ongoing environment for high-yield savings accounts presents a valuable opportunity for consumers to significantly grow their wealth.

By diligently Comparing U.S. High-Yield Savings Accounts, individuals can secure advantageous rates that outpace inflation and enhance their financial security. The key is to remain informed, adaptable, and proactive in managing your savings portfolio.

Monitoring economic indicators and banking trends will be essential to capitalize on the best offerings for high-yield savings accounts, ensuring your money works harder for you in the years to come.